.png)

Mastering PPh 21 and PPh 23: 10 Monthly Tax Filing Rules to Protect Your Business

Introduction: Why Monthly Tax Filing Matters

For any legally established business in Indonesia, staying compliant with tax obligations is not just a formality—it’s a critical part of responsible and sustainable operations. The Indonesian tax system imposes specific monthly filing requirements that all companies must meet, regardless of their income status.

Two of the most commonly encountered tax types are PPh 21 and PPh 23. These income-based taxes are mandatory for businesses that hire employees, contract vendors, or make service payments to individuals and companies. While they may seem similar, they have very different scopes and rules. PPh 21 and PPh 23 must be filed and paid monthly, even when there are no transactions—failing to do so could invite penalties.

The consequences of non-compliance include administrative fines, interest charges, and, in some cases, the suspension of your business’s NPWP (Nomor Pokok Wajib Pajak or tax identification number). Once suspended, a business can lose access to various permits, contracts, and financial services, severely hampering operations.

This article serves as a practical guide to help foreign and local businesses alike navigate PPh 21 and PPh 23 in Indonesia. Whether you’re managing payroll or contracting third parties, understanding these tax rules will protect your company from unexpected setbacks and legal risks.

What Is PPh 21 and PPh 23?

Understanding PPh 21 and PPh 23 is crucial for every business operating in Indonesia. These are two types of withholding taxes—meaning, the company is responsible for calculating, deducting, and submitting them to the government on behalf of others.

PPh 21 applies to income earned by individuals, primarily in the form of salaries, wages, honorariums, allowances, and other compensation. This tax is calculated progressively based on an individual’s gross income, with rates ranging from 5% to 35%, depending on income brackets. For example, a full-time employee with a monthly salary exceeding certain thresholds will be subject to higher PPh 21 deductions. Bonuses, THR (religious holiday allowances), and overtime are also subject to PPh 21.

In contrast, PPh 23 is imposed on payments made for services rendered, including consulting, legal assistance, management, design, rental of assets, dividends, royalties, and interest. It applies to both individuals and companies. The rate is usually 2% for most service transactions and 15% for payments like dividends or royalties. Unlike PPh 21, PPh 23 is a flat rate, regardless of the recipient’s income level.

The key difference between withholding taxes like PPh 21 and PPh 23 and regular income tax is who holds the responsibility. In this case, the business is the withholding agent. You don’t just pay your own taxes—you also handle taxes on behalf of employees and service providers. This makes businesses legally accountable for collecting the correct amount and submitting it on time.

Failing to fulfill these obligations doesn’t just impact the recipient—it puts your company at risk of audits, penalties, and reputational harm. Whether you’re managing payroll or engaging third-party vendors, staying on top of PPh 21 and PPh 23 ensures your operations remain compliant and protected under Indonesian law.

Who Must File PPh 21 and PPh 23?

All registered business entities in Indonesia—including PT (Perseroan Terbatas), PT PMA (foreign-owned companies), and CV (Commanditaire Vennootschap)—are required to file PPh 21 and PPh 23, regardless of their size, revenue, or level of activity.

This obligation applies equally to foreign-owned entities (PT PMA), even if the company is not yet generating income or profit. As long as the company is legally established and holds a Taxpayer Identification Number (NPWP), it must fulfill its monthly tax obligations.

For example:

- A PT PMA that pays salaries or allowances to local or expatriate staff must file and pay PPh 21 every month.

- If the same company pays for IT support, marketing consultants, or legal services, it must withhold and report PPh 23 on those payments.

Even if no transactions take place in a given month, businesses are still required to submit a “Nihil” (zero) report. This report confirms that there was no taxable event but proves continued compliance with Indonesian tax laws.

Neglecting to file these reports, even when there is no tax to be paid, can lead to administrative penalties and a negative mark in the company’s tax history. For PT PMAs, this may also complicate future licensing renewals, visa applications, or bank interactions.

In short, PPh 21 and PPh 23 are not optional filings. They are mandatory for all active tax IDs. Staying compliant isn’t just about avoiding fines—it’s about maintaining good legal standing as a responsible business in Indonesia.

Monthly Filing Deadlines & Procedures

Understanding the monthly filing deadlines for PPh 21 and PPh 23 is essential to avoid unnecessary fines and maintain compliance with Indonesian tax regulations. Both taxes follow a similar timeline but differ slightly in how they are reported.

For PPh 21 (income tax on salaries and employee benefits):

- Payment Deadline: The 10th day of the following month

- Filing Deadline: The 20th day of the following month

For PPh 23 (withholding tax on services, dividends, royalties, rent, etc.):

- Payment Deadline: Also the 10th of the following month

- Filing Deadline: The 20th of the following month

All tax payments must be made through a tax payment code (Kode Billing), and reporting must be completed using the DJP Online system or the e-Bupot system (electronic withholding tax system) for eligible taxpayers.

For example, if a company pays staff salaries and engages a digital marketing consultant in January:

- The PPh 21 and PPh 23 payments must be made by February 10th.

- The tax return filings must be completed by February 20th.

Failure to meet these deadlines results in penalties, including:

- 2% interest per month of the unpaid tax amount

- Administrative fines, ranging from IDR 100,000 to IDR 1,000,000, depending on the type of report and the nature of the non-compliance

These penalties apply even for late submission of “Nihil” reports, which are mandatory even if no transactions occurred.

In short, timely filing and payment of PPh 21 and PPh 23 not only help businesses stay compliant but also protect their reputation and avoid financial losses due to fines. Setting up monthly reminders or working with a trusted tax consultant can make a significant difference.

Common Errors and How to Avoid Them

Even well-meaning businesses can face tax trouble due to common mistakes in handling PPh 21 and PPh 23. These errors can lead to audits, penalties, and significant financial risk. Understanding them is the first step to prevention.

One of the most frequent issues is misclassifying payments. For example, treating an independent contractor as a full-time employee may result in wrongly applying PPh 21 instead of PPh 23. Each type of payment has specific tax obligations, and misclassification can trigger compliance issues during audits.

Another frequent error is failing to withhold PPh 23 from vendor invoices. If your business pays for consulting, IT services, or design work, you are legally required to withhold and report PPh 23—regardless of whether the vendor reminds you. Forgetting to do so makes your company liable for the full tax, plus interest.

Some businesses also skip reporting during months without transactions. However, “Nihil” (zero) reporting is still mandatory for both PPh 21 and PPh 23. Skipping these reports may flag your company for non-compliance.

Additionally, not keeping supporting documents—such as invoices, contracts, or proof of tax payment—can weaken your position during tax audits. Proper documentation is essential to justify your filings and protect your business.

Failing to comply with PPh 21 and PPh 23 obligations can result in back taxes, interest charges, and fines. To avoid these issues, establish clear internal processes, educate your finance team, and consider working with a professional tax advisor.

Tools and Systems to Simplify PPh 21 and PPh 23 Filing

Filing PPh 21 and PPh 23 doesn't have to be complicated—especially if you're using the right tools. In Indonesia, several digital platforms and systems are designed to help businesses stay compliant and efficient with their tax obligations.

DJP Online is the official government portal where registered taxpayers can submit monthly reports, including PPh 21 and PPh 23 filings. It’s free, widely used, and supports "Nihil" submissions when no transaction occurs.

For companies dealing with service transactions, e-Bupot Unifikasi is a key platform. It allows you to generate withholding tax certificates, upload e-invoices, and file reports all in one place. This system is especially helpful for businesses that must withhold PPh 23 from vendors.

To streamline the process even further, many businesses integrate with third-party tax software like OnlinePajak and Mekari Klikpajak. These platforms offer automation, real-time calculations, and easier compliance tracking, especially if you're managing high transaction volumes.

Having a certified tax consultant or in-house accounting team can elevate your tax reporting quality. They help classify transactions correctly, file on time, and manage exceptions—reducing your audit risk and ensuring your PPh 21 and PPh 23 filings are always accurate.

With the right tools and expert support, managing monthly taxes becomes much more manageable—and less stressful.

How to Calculate PPh 21 and PPh 23: Examples

Understanding how PPh 21 and PPh 23 are calculated is essential for accurate reporting and avoiding unnecessary fines. Below are practical examples to help you grasp the basics.

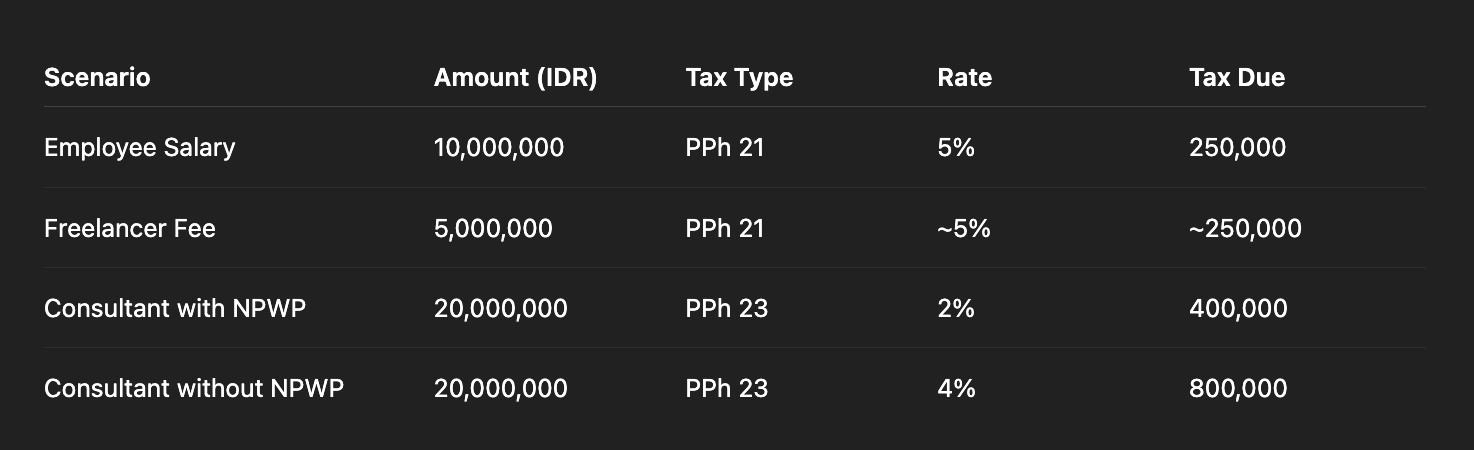

PPh 21: Employee Salary Breakdown

Let’s say an employee earns IDR 10,000,000/month and is unmarried with no dependents. The annual income is IDR 120,000,000. After deducting PTKP (Penghasilan Tidak Kena Pajak), assume the taxable income is IDR 60,000,000.

Tax rate:

- 5% for income up to IDR 60,000,000

- PPh 21 = 5% x IDR 60,000,000 = IDR 3,000,000/year or IDR 250,000/month

The company must withhold and report this amount each month.

PPh 21: Freelancer/Contractor

Freelancers paid IDR 5,000,000/month without employment status are also subject to PPh 21. If the fee includes tax (gross-up method), a 50% norm is used, and tax is calculated progressively. In most cases, it results in roughly 2.5%–5% effective tax.

PPh 23: Service Vendor (Consulting Fee)

A PT PMA pays an IT consultant IDR 20,000,000 for services.

- PPh 23 rate = 2%

- Tax withheld = 2% x IDR 20,000,000 = IDR 400,000

The company must pay this tax to the state and issue a Bukti Potong (withholding receipt) to the vendor.

Important Note: If the vendor doesn’t have an NPWP, the tax rate increases by 100%. So, the PPh 23 would be 4% instead of 2%.

By mastering how to calculate PPh 21 and PPh 23, your company can ensure full compliance, proper withholding, and accurate reporting every month.

PPh 21 and PPh 23 in Annual Tax Reconciliation

While monthly tax filings are mandatory, they are not the final step. At the end of each fiscal year, businesses must reconcile all tax payments, including PPh 21 and PPh 23, through the Annual Tax Return (SPT Tahunan).

For PPh 21, companies must submit employee salary summaries and total tax withheld throughout the year. This data must match what was reported monthly and what employees file individually. Any discrepancy can trigger tax audits or penalties.

For PPh 23, the company must include all relevant Bukti Potong (withholding receipts) as proof of tax paid to vendors or freelancers. These documents are crucial in validating expenses and deductions during the corporate annual report.

The reconciliation process ensures that all withheld and prepaid taxes are correctly reported, aligning monthly filings with the annual return. Failure to reconcile PPh 21 and PPh 23 accurately may result in underpayment issues, fines, or delayed processing of refunds.

To stay compliant and avoid red flags, businesses should regularly audit their monthly reports and coordinate with tax consultants before submitting their annual SPT.

Final Tips for Long-Term Compliance

Maintaining long-term tax compliance in Indonesia requires consistency, accuracy, and routine checks. Always submit your monthly tax filings—even if your report is nil—to avoid automatic fines or flags in the DJP system.

Keep your payroll data and vendor database up to date, including changes in employment status, NPWP numbers, or contract details. Use a tax calendar to track important dates, especially the 10th and 20th of each month.

Most importantly, consider partnering with a certified tax advisor who understands the nuances of PPh 21 and PPh 23. Their guidance can help you stay compliant, prevent audit risks, and streamline your annual tax reconciliation.

By adopting these habits, businesses can ensure smooth operations, avoid penalties, and build a strong compliance record with the Indonesian tax authority.

Source:

FAQ

Share the blog

Related News

SYNERGY PRO Business & Legal Consulting

Social Media